Robinhood Stock Forecast as a Key Metric Jumps to $31 Billion in 3 Years

- Views: 4

This post was originally published on this site

HOOD shares slid after a weak crypto quarter, but retirement assets surging to $31 billion and accelerating growth in options, futures, and prediction markets paint a more nuanced — and potentially bullish — picture.

Robinhood Markets (NASDAQ: HOOD) finds itself at a crossroads that is becoming increasingly familiar for high-growth fintech companies: the headline numbers disappoint, yet beneath the surface, structural momentum quietly continues to build. Following the publication of its first-quarter 2026 results, HOOD shares suffered a sharp decline, closing the week at $73.66 — a steep retreat from the 52-week high of $154. And yet, for investors willing to look beyond the noise of a single quarter, the underlying story is considerably more compelling.

The pivot point of the latest earnings miss was not buried in obscure footnotes. Crypto revenue — once one of Robinhood’s most potent growth engines — plunged to $134 million in Q1 2026, down from $268 million in the prior year. With Bitcoin and major altcoins trading in an unusually narrow range throughout the first quarter, transaction volume across the crypto segment fell substantially. Analysts had anticipated some softness, but the magnitude of the decline was enough to rattle investor confidence and trigger a sharp down-gap on the daily chart.

But to read Robinhood’s story through the lens of crypto alone is to miss a more important narrative about transformation, diversification, and long-term positioning.

The Retirement Revolution: $31 Billion in Three Years

Perhaps the most striking data point to emerge from the company’s latest disclosures did not come from the earnings report itself, but from an X post by CEO Vlad Tenev. Retirement assets under custody have surged to $31 billion — a milestone reached in just three years since the product launched. The Q1 2026 report had disclosed assets under custody at $27.4 billion, meaning the figure climbed by an additional $3.6 billion in a matter of weeks.

The retirement segment’s growth is being driven by more than market appreciation. The number of active retirement accounts rose 50% to approximately 1.98 million — a figure that underscores how effectively the company is converting platform engagement into long-term, sticky assets. Unlike trading revenue, which ebbs and flows with market sentiment and crypto cycles, retirement assets represent a durable, compounding base that strengthens the business regardless of what any given quarter’s trading volumes look like.

Adding further tailwinds is Robinhood’s selection to participate in the Trump accounts programme, a savings initiative proposed under the so-called Big Beautiful Bill. Under the scheme, parents can invest in accounts on behalf of their children, with corporate participants like Michael Dell committing $250 per account. While this has weighed on near-term earnings as the company ramps up operational infrastructure, the long-term economics of acquiring young, generational investors at scale could prove transformative.

Robinhood retirement growth continues

Options, Futures, and Predictions: Where the Real Growth Is

While the crypto shortfall grabbed headlines, several other business segments delivered numbers that would be the envy of most financial platforms. Futures contracts traded on the platform surged to 20.1 million in Q1 2026 — a remarkable leap from just 3.4 million in the same period last year, representing nearly a sixfold increase year-over-year. Index options contracts climbed to 29.4 million from 10.4 million, roughly tripling over twelve months.

These are not marginal improvements. They are the hallmarks of a platform capturing genuine market share in some of the fastest-growing corners of retail financial services. Sophisticated retail investors, once the exclusive domain of full-service brokers and institutional platforms, are increasingly migrating to Robinhood’s streamlined, mobile-first interface.

The prediction marketplace is another standout. The platform executed 8.8 billion event contracts in Q1 2026, up from 8.5 billion in Q4 2025 — and a world apart from the 0.3 billion processed in the same quarter of 2025. Management has signalled that this division is poised to accelerate further, particularly as the United States moves toward its 2026 midterm elections, which historically drive significant user engagement in political prediction markets.

Valuation: A Tale of Two Frameworks

At $73.68, HOOD shares sit at an intriguing juncture in the valuation debate. The stock carries a market capitalization of approximately $65.6 billion on revenues of $4.6 billion — a premium multiple that reflects high growth expectations, but one that is also vulnerable to earnings disappointments like the one just delivered.

Bullish narratives peg fair value at approximately $194.61 per share, implying the stock is deeply undervalued at current prices. That view leans on strong profitability momentum, rich user monetisation metrics, and ambitious assumptions around Robinhood’s emerging tokenisation of traditional assets — a product CEO Tenev has described as the biggest innovation the industry has seen in a decade. For Q2 2025, total revenues had already jumped 45% year-over-year to $989 million, with net income surging 105% to $386 million, demonstrating the underlying earnings power of the platform when conditions cooperate.

However, more conservative discounted cash flow models offer a sobering counterpoint. Certain DCF frameworks estimate HOOD’s intrinsic value based on future cash flows at just $44.76 per share — implying the stock is meaningfully overvalued even at its post-earnings beaten-down level. The divergence between these two frameworks is unusually wide, and that itself tells a story: Robinhood is a company where assumptions about growth trajectory, margin expansion, and regulatory risk can produce wildly different outcomes. Tighter regulation of crypto and tokenisation remains the most material downside risk to the bullish case.

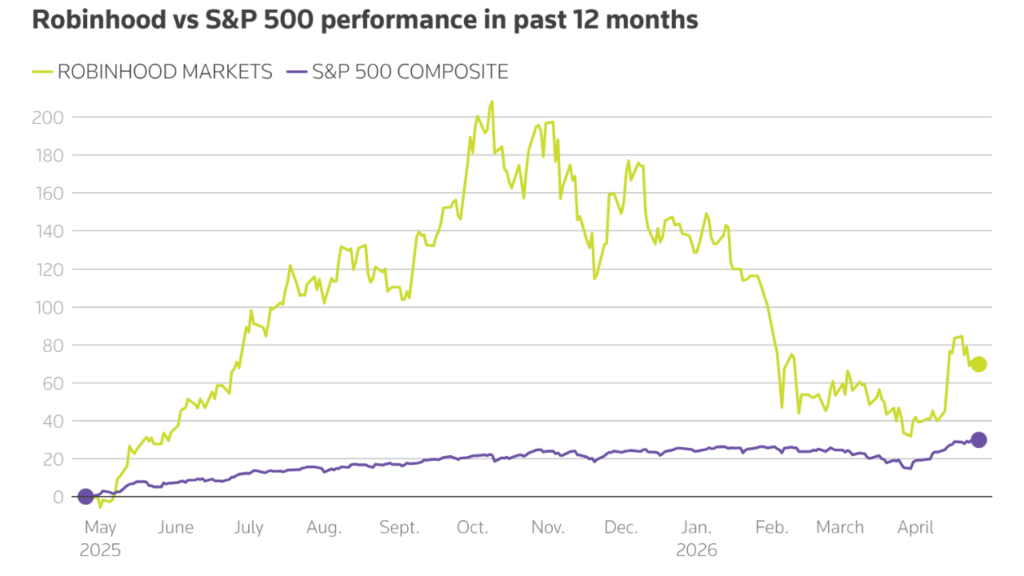

Robinhood vs S&P 500 performance in past 12 months (Source: Reuters)

Technical Picture: Support Holds, Eyes on $100

From a technical standpoint, HOOD is navigating a delicate moment. On the 1-minute intraday chart as of May 3, 2026, the stock is trading at $73.68 — below all four key exponential moving averages, which are stacked between $73.95 and $74.41 and beginning to curl downward. That EMA cluster now acts as immediate overhead resistance, and the latest candle arrived on a sharp volume spike of 28.66K, suggesting sellers remain in control of the near-term tape.

Zooming out to the daily picture, the post-earnings down-gap dropped the stock toward the key support level of $65.47, which marked the March 2026 low. This zone remains the line in the sand for bulls — a decisive close below $65 would invalidate the current bullish reversal setup and open the door to a deeper drawdown.

On the constructive side, the daily chart has formed a megaphone pattern — a structure defined by diverging ascending and descending trendlines that often precedes a powerful reversal when it resolves to the upside. The down-gap left behind after earnings also tends to act as a price magnet, with stocks frequently staging a rally to fill the void. For that recovery to gain credibility, HOOD first needs to reclaim the $74.41 level — the 200 EMA on the intraday chart — before targeting the psychological resistance at $100. A move above last month’s high of $92 would serve as the key confirmation signal for bulls on the longer-term thesis.

Robinhood daily stock chart (Source: TradingView)

The Bottom Line

Robinhood’s Q1 2026 results were, on balance, a disappointment — but the story they tell is more complex than the share price decline suggests. The crypto headwind is real, but it is cyclical. The structural achievements — $31 billion in retirement assets in just three years, near-sixfold growth in futures volumes, a tripling of index options contracts, and an expanding prediction marketplace — speak to a platform broadening its economic foundation in ways that matter for the long term.

The consensus among analysts projects Q2 2026 revenue of $1.19 billion, representing approximately 20% growth, with full-year revenues growing 13% before accelerating to 20% in 2027 and reaching $6.07 billion. For patient, conviction-driven investors, the risk-reward on HOOD at current levels appears more interesting than the headline drop implies. Whether the stock can reclaim $92 — let alone the analyst bull-case territory — will ultimately depend on how effectively management executes on an ambitious product roadmap that is already showing early signs of delivering.

The post Robinhood Stock Forecast as a Key Metric Jumps to $31 Billion in 3 Years appeared first on NFT Plazas.

You Might Like